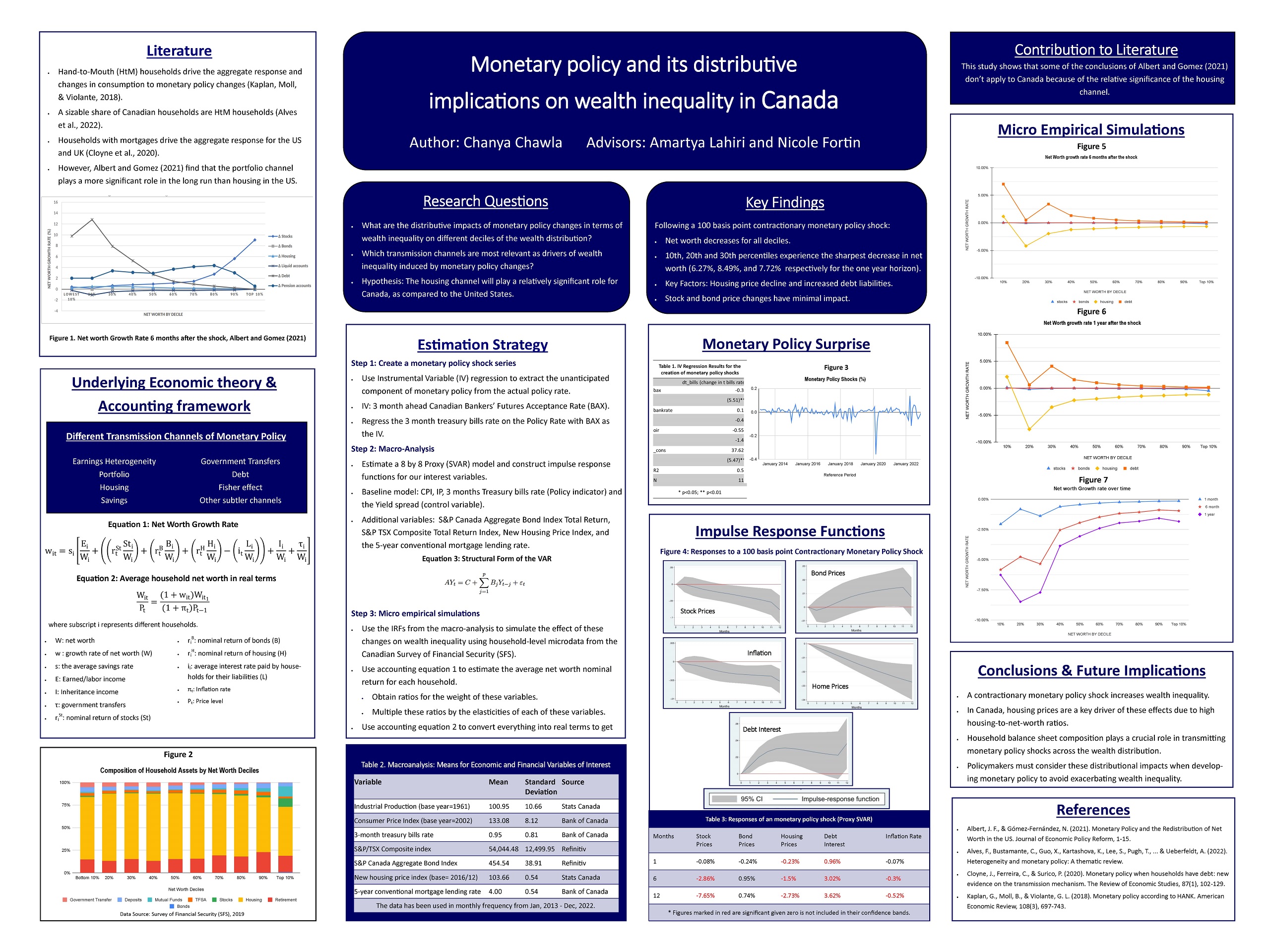

The aim of this paper is to investigate the distributive effects of monetary policy on wealth inequality, with a focus on the Canadian context. While most recent literature acknowledges the distributive implications of monetary policy changes on wealth inequality, most recent studies use data from the United States and the United Kingdom. Therefore, this research hopes to further explore the relationship between monetary policy and wealth inequality in the Canadian context. This research adopts a two-step approach, drawing from similar studies in the field, that includes both macro and micro analyses. The macro analysis involves estimating a Proxy Structural Vector Autoregression (SVAR) model using various monetary and financial indicator variables to measure the impacts of monetary policy shocks on key financial and real variables. The results of the macro analysis are then combined with household-level microdata to simulate the effect of these changes on household balance sheets over three different time horizons. The findings suggest that wealth inequality increases after a contractionary monetary policy shock, with the effects becoming more pronounced over time. The study highlights the role of housing prices and debt in driving these distributional impacts in Canada, with stocks having a relatively lower impact.

The aim of this paper is to investigate the distributive effects of monetary policy on wealth inequality, with a focus on the Canadian context. While most recent literature acknowledges the distributive implications of monetary policy changes on wealth inequality, most recent studies use data from the United States and the United Kingdom. Therefore, this research hopes to further explore the relationship between monetary policy and wealth inequality in the Canadian context. This research adopts a two-step approach, drawing from similar studies in the field, that includes both macro and micro analyses. The macro analysis involves estimating a Proxy Structural Vector Autoregression (SVAR) model using various monetary and financial indicator variables to measure the impacts of monetary policy shocks on key financial and real variables. The results of the macro analysis are then combined with household-level microdata to simulate the effect of these changes on household balance sheets over three different time horizons. The findings suggest that wealth inequality increases after a contractionary monetary policy shock, with the effects becoming more pronounced over time. The study highlights the role of housing prices and debt in driving these distributional impacts in Canada, with stocks having a relatively lower impact.

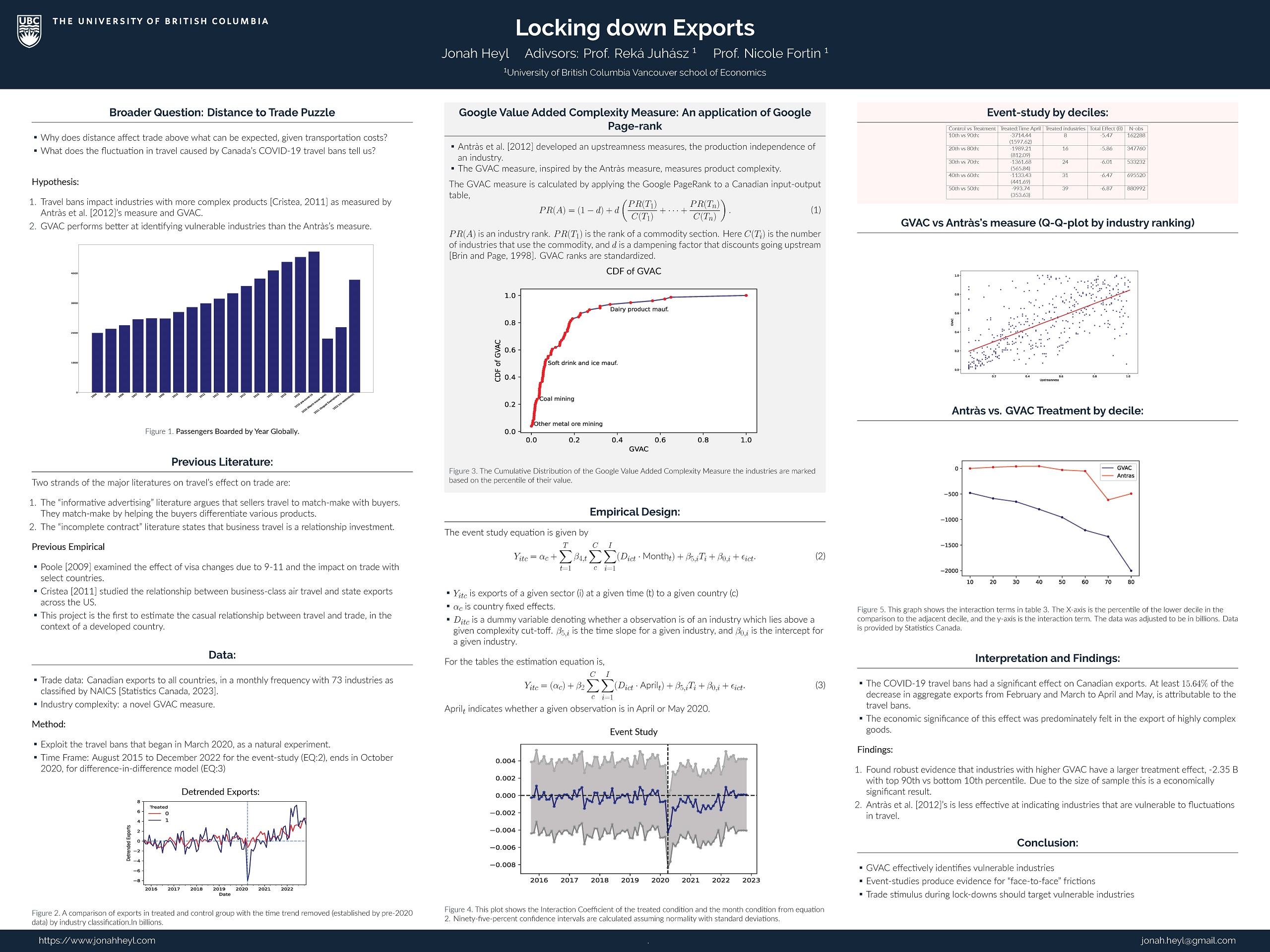

Canadian exports dropped by nearly 30 % in March of 2020 before shapely recovering. Which industries were most impacted, and how can the government smooth-out export shocks? To examine the first question, I develop a novel measure of industry complexity based on centrality in inter-industry flows. Using a sample of Canadian export data to all countries, I show that the top decile of complex industries experienced a 5.47 B (CAD) decrease in exports over the bottom decile in industries. Using multiple event studies, I show that the GVAC outperforms the literature’s foremost measure of identifying vulnerable industries.

Canadian exports dropped by nearly 30 % in March of 2020 before shapely recovering. Which industries were most impacted, and how can the government smooth-out export shocks? To examine the first question, I develop a novel measure of industry complexity based on centrality in inter-industry flows. Using a sample of Canadian export data to all countries, I show that the top decile of complex industries experienced a 5.47 B (CAD) decrease in exports over the bottom decile in industries. Using multiple event studies, I show that the GVAC outperforms the literature’s foremost measure of identifying vulnerable industries.